Here's a look at three recent innovations in home security.

A home security system could make you eligible for a property insurance discount, too. Get in touch today to discuss your policy or anything else

0 Comments

As a seasoned homeowner, you’ve been paying off your mortgage and are now considering buying a second home – a place you can retreat to on vacation, an investment property, or maybe even a combination of the two. You’ve been through the home-buying process before so you know what to expect, but there are certain factors unique to buying a second home that you'll want to consider. These factors will vary depending on how you intend to use the property, so it's a good idea to determine if the home will be for mostly personal use or if it will be occupied by tenants.

Here are six essential things you should consider before buying a second home: 1. Can I Afford It? It may seem like an obvious question, but can you afford a second home? If you choose to take out a mortgage on a new property, take some time to carefully understand the requirements so you’ll be better prepared for the process when submitting your mortgage application. As a homeowner, you're probably well aware of the strict credit requirements for taking out a mortgage, and things get even more serious when it comes to buying a second home. Your debt-to-income ratio will, of course, be a significant factor, and when it comes to holding two mortgages, you may find it a bit more challenging to balance this ratio. Also, be prepared to shell out a hefty amount for a down payment, since you'll be required to put at least 10 percent down on a vacation home and perhaps an even higher amount if it will be used as an investment property. And don’t forget that a second home will need to be protected, so you’ll want to talk to your homeowners insurance agent about getting a quote, once you’ve got your sights set on a second property to call your own. 2. How Will It Affect My Taxes? Understanding the tax implications of your new property will be another challenge. If you intend to rent your place to tenants, that means you'll earn rental income throughout the year, and that income will be taxable. As the owner of the home, you also may be able to take deductions in the form of mortgage interest, property taxes, repairs, depreciation, and operating expenses. One of the most important things to do as the landlord is to maintain accurate records of your income and expenses throughout the year in order to properly report the information on your tax return. 3. What Home Expenses Should I Expect? Just like your primary residence, your second home will also require you to shell out cash for expenses – both expected and unplanned. It’s helpful to have a budget set up for home needs, and with two homes, this may be an even more critical step, since your expenses will be elevated. In addition to the maintenance costs, remember you'll have property taxes, insurance, potential homeowners' association dues and more. If the property is at the beach or in a flood zone, you'll also need to consider things like flood insurance in addition to your regular homeowners policy. And finally, if you plan to rent the property, you'll also need to look into insurance that specifically protects you as a landlord. Travelers wants to help you protect the things that matter to you. We offer a wide breadth of products so you can be covered at home and on the road. 4. How Will I Use the Property? If the property will solely be used for personal vacations, this question isn't as critical. However, if you intend to rent the home occasionally or full time, you'll want to consider your strategy ahead of time. Keep in mind that for mortgage purposes, your lender doesn't consider the income generated from renting the home. Whether you can afford the second property is determined solely based on your credit and debt-to-income ratio. If you plan to rent the home, it's important to build your rental strategy as early in the process as possible to ensure you'll have rental income that can help offset the home's monthly expenses from the start. That will translate to less cash out of your pocket, as long as the tenants are diligent in paying the rent on time. 5. Who Will Maintain the Property? You’ll want to plan for who will maintain the property to protect your investment. If the investment property is located near your primary home, it may be easy for you to provide the regular maintenance and upkeep of the home, if you’re handy and have the time – and the will – to do those tasks. However, if the property is far from your primary home, you'll need to think about how it will be cared for when you're not staying there. This is especially important if the property is located in an area that’s susceptible to strong storms and hurricanes. Severe weather events can pop up at a moment's notice, and your second home will need to be properly prepared to withstand such weather. If the home will be for your personal use, perhaps you can find a neighbor to keep an eye on the house when you're not there. If you plan to rent the home, consider hiring a rental management company to take care of the general upkeep so you won't have to worry about every little detail from afar. 6. Is the Property in an Ideal Location? Whether buying a second home for your personal enjoyment or as an investment property, make sure you choose the right location for your needs. You may not get as much use as you’d like from a vacation home that requires extensive travel to get there. And, a rental home in an unpopular locale may lead to months of being unoccupied – which means you’re paying the second mortgage yourself rather than with income from renting it out. In either scenario, ensuring the home is in an ideal area can help provide you with a positive return on investment. If you do intend to rent the property, take some time to research the rental climate in the area before moving forward. The best places to own investment property are often popular vacation destinations and cities with an abundance of career options. Buying a second home doesn't have to be daunting. In fact, with careful research and planning, it can be a smart investment for your future.  Do you know where most home fires start? If you guessed the kitchen, you’re right. One of the most popular rooms in the house also has the potential for danger. But a few simple habits can help prevent damaging fires from ever starting in the first place. To find a little more peace of mind this season, here are four ways to make your home safer. 1. Don’t walk away from an active stove. Unattended cooking is a leading cause of kitchen fires. If you need to leave while frying, grilling or broiling, make sure to turn your stove off first. It’s easy to lose track of time when you step away to answer the door or check on the kids, and it doesn’t take long for trouble to start. 2. Keep clutter under control. It’s not uncommon for kitchen counters to get loaded up with stuff. Make it a priority to clear your kitchen countertops of anything flammable, such as wooden utensils, papers and dish towels, especially around the stove. 3. Use space heaters, fireplaces and woodburning stoves safely. If you use a space heater during colder months, consider replacing older models with one designed to turn off if it tips over. Position space heaters with a 3-foot distance from everything else and always turn them off before you leave the house or go to sleep. If your home has a fireplace or wood-burning stove, have it inspected annually by a professional. Use a mesh screen to keep sparks inside the fireplace. 4. Practice candle safety. As with a stove, a lit candle is an active fire that you shouldn’t leave unattended. Blow out candles before leaving a room and keep burning candles on level surfaces and away from flammable objects, young children and pets. Have questions about your insurance coverage? Reach out and we’ll be happy to help.  Car insurance is a necessary expense for many people, and there are a variety of ways to save on this household cost once you know what it takes. To get started, gather your personal information, determine your budget and then consider the insurance coverage that you think will best safeguard you and your lifestyle.

Here are 10 ways to save on your car insurance: 1. Gather Specifics About Your Car and Its Primary Drivers One way to begin the process of shopping for car insurance to get the most value for your money is to gather all of the information an insurance carrier needs to offer you the best possible rate.1 Start by compiling this basic information before you shop for quotes:

With this information, an insurance carrier can suggest the best coverage and rates for you and your lifestyle. 2. Research How Much Car Insurance Costs Before You Buy or Lease When you buy or lease a car, it can be tempting to get a brand-new car or trade in your practical family vehicle for a sports car. Just keep in mind that the type of car you drive may impact your insurance coverage and rate. Be sure to check the cost of insurance before you finalize your car purchase or lease. Insurance rates may vary widely depending on the type of car, repair costs, safety record and many other subjective points.2 3. Research All Car Insurance Coverage Requirements Each state has specific requirements for car insurance coverage.3 Coverage may become more complicated when a financial institution owns the vehicle you drive, so if you’re taking out a loan to make the car purchase, keep in mind that the lender may require you to have specific insurance that might otherwise be optional.4 One example is collision insurance that pays for the repairs of damage to your car sustained during an accident. Another example is comprehensive coverage, which typically covers the loss of the car for theft, fire and other damage due to non-accidents. Find out what coverage you need and the cost before you buy or lease. 4. Decide What Additional Coverage You Need It may seem counter-intuitive but buying additional car insurance coverage may save you money. Weighing the options for additional coverage will help you to ensure you are well protected. Consider how your finances might be impacted if you're involved in an accident, and the injuries or damages exceed the amount covered by insurance. You purchase car insurance to help protect against the potential costs of a theft or accident, so be sure to talk to your insurance agent or carrier for professional guidance on the appropriate level of coverage for you. In addition, there are other coverage options that may save you money. What if your financed car is totaled? Can you afford to pay the entire loan? In this case, you may want to consider GAP insurance, which covers the difference between what your vehicle is currently worth, which is what your standard insurance typically will pay, and the amount you owe on it. Again, your insurance agent or carrier can help guide you through the available options. 5. Save Money with Accident Forgiveness Having a clean driving record is one thing that typically can help you to qualify for lower premiums. But there are times when even a good driver can have an accident. You may want to consider looking into potential savings through Accident Forgiveness and Minor Violation Forgiveness, if available in your state. These optional features can help you avoid a premium increase following your first covered accident or minor violation. There are also other features that can help provide peace of mind, such as Decreasing Deductible and a Total Loss Deductible Waiver. Ask your insurance agent about these plans, if you fit the bill as being a responsible driver because of your good driving record. Some carriers – in select states – also offer a program that uses smartphone technology to capture and score driving behavior of drivers covered on your policy, which could result in savings both in your first term and at renewal. It’s another option to explore when you’re a good driver and looking to save on your car insurance. 6. Determine What Car Insurance You May Not Need If you own an older car and are looking to trim your expenses, you may consider dropping collision and comprehensive coverage. You’ll want to consider how much your older car is worth when you consider the cost of your premium including collision and comprehensive coverage. Be sure to also consider your individual driving situation to base your cost-cutting efforts on all the factors that could help you determine if this is a wise choice for you. With an older car, you may be paying premiums that total more than your car's value. Typically, if your car is worth less than 10 times the insurance premium, it may not be cost effective to keep that part of your coverage. 7. Life Cycle Events Can Save Car Insurance Costs One thing you can count on is that life will sometimes bring changes in your lifestyle and circumstances, so it’s smart to consider how these changes may or could affect your car insurance costs. For example, did your child go away to school? Perhaps there’s a Student Away at School discount you can explore. Did you buy a home? Maybe you can explore a Multi-Policy Discount and get the benefit of bundling your policies. These are some of the events that may help lower your car insurance rate. It’s a good idea to notify your car insurance agent when you have a major life event such as these, to have a conversation to ensure you’ve got the best coverage for your current life needs. 8. Choose the Deductible That Is Right for You Your car insurance deductible is the amount you’ll pay out of pocket before your insurance kicks in. The lower the deductible, the less you’ll pay out of pocket if an accident occurs. Selecting a higher deductible may lower your car insurance premiums. For example, if you choose a $1,000 deductible and have an accident causing $2,000 in damage, you would pay the first $1,000 of a covered loss before insurance kicks in. 9. Compare Car Insurance Companies and Costs With many things we buy nowadays there are choices. Many of us wouldn't think of buying a product or service without comparing prices, the value you get for your money, and the reputation of the provider. You may want to consider using the same philosophy when you purchase car insurance. Do your homework and then talk to your insurance agent or carrier about what your needs are.8 10. Ask Your Agent About Available Discounts It’s a good practice to check in with your insurance agent at least annually to find out if you are eligible for a better car insurance rate. You may receive discounts if you bundle coverage, such as buying insurance for your home and car from the same company. As mentioned earlier, safe driving records and extra safety features on a car may also lower rates. Ask your insurance agent about any new offerings or gaps in your coverage to determine the best coverage for you. Now that you’ve got some ideas on how to save on your car insurance, you may want to check with your carrier to review your coverage.  What’s your biggest challenge at home? For many of us, it’s a lack of space.

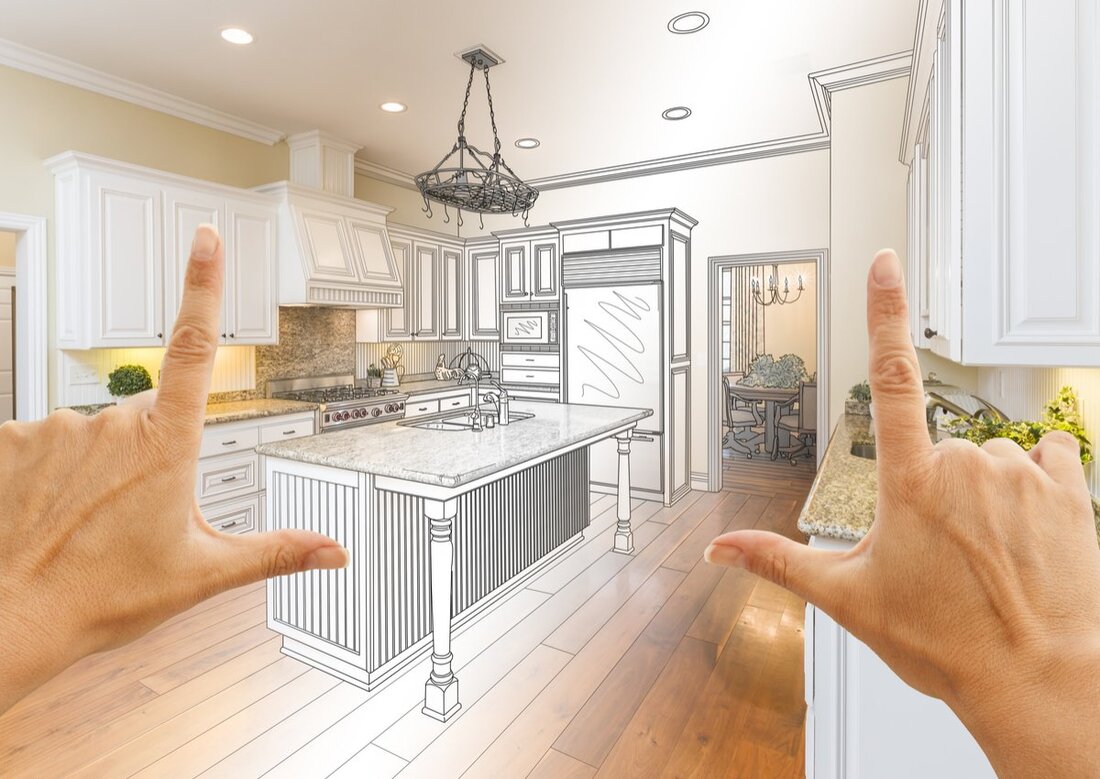

So how can you carve out an extra bedroom, a home office or a study nook for a school-age child? The answer may not be as out-of-reach as you think. Here are four solutions for a range of spaces and budgets. 1. Transform the Garage Are you wishing for a home gym, an artist’s cottage, an office, a family room, an in-law suite or a rental apartment? Your garage may be the answer. Both attached and unattached garages can be converted into an extra room. To get started, research local building codes and zoning ordinances. If you belong to an HOA, you’ll need to check their rules, too. If you’re doing more than small cosmetic changes, it’s also a good idea to consult with a professional architect, engineer and contractor. 2. Consider a Prefab Shed Modern and inviting, a prefab shed is an easy way to add a room if you don’t have a garage to work with. And unlike with a garage remodel, you may not need a permit for installation. 3. Convert the Attic or Basement As with a garage, an attic or basement could be remodeled into an inviting living space for a variety of uses. Consider adding a half-bath and/or kitchenette if you have the budget and want to create an in-law suite or apartment. 4. The “No-Remodel” Option Finally, there are less expensive and invasive ways to create more space in your home. With more people working remotely, closet offices have become popular. Scan your space for any closets and corners where clutter has accumulated. How could these nooks be put to better use? Have questions about your insurance coverage? Is there anything else we can help with? Reach out anytime.  This may sound obvious, but selling a house sometimes comes down to just how appealing your home is to potential homebuyers. The attributes that make your house attractive to buyers can include price, the condition of your home and its curb appeal, as well as details like the number of bathrooms, bedrooms and whether the home appears dated. Discerning buyers typically want to walk into a house and immediately feel at home. How quickly you sell your home ‒ and at what price ‒ may depend on your ability to create that I’m-already-at-home feel.

Here are 10 easy home remodeling ideas that can help transform your home sweet home to the gotta-have-it house of your buyer’s dreams. 1. Replace the garage door. The surprise most home sellers discover ‒ often too late ‒ is that most sellers won’t fully recoup the cost of a renovation when they sell their home. When it comes to getting some bang for your renovating buck, however, the garage door is one suggestion to consider; it also can give a boost to your home’s curb appeal. 2. Upgrade the front door. A relatively inexpensive yet effective home improvement idea is a new front door ‒ one of the first things a home shopper will notice when they view online photos or arrive for a showing. For example, a new steel door can be both eye‒catching and energy efficient ‒ a boon for cost-conscious buyers-to-be. Or you could consider the pricier installation of a grand entrance ‒ perhaps a new front door with dual skylights ‒ which can help increase the attraction from upscale buyers. 3. Re-face the house. Another way to help increase your home value is by improving the exterior of your home. A good pressure washing may cost a few hundred dollars and can reduce or remove the unsightly dust, grime and mildew that often clings to exterior siding. For a house with more exterior wear, new siding is a pricey project but one that can help add a dramatic boost and take years off your home’s exterior appearance. 4. Maintain your lawn and refresh landscaping. You only have one chance to make a great first impression ‒ which is why renovations affecting curb appeal make our list. Home improvements that help add value and appeal to buyers include standard lawn care and landscape maintenance. Consider it a smart investment that can eventually turn out to be money well spent when you’re prepping your house for sale. 5. Refresh the kitchen. For many homeowners, the kitchen is where guests and family gather, making it one of the top house renovation ideas that come to mind when preparing a home for sale. Still, a major kitchen renovation may not be worth the cost when it comes time to sell; however, smaller, cost-effective upgrades can help make the kitchen more attractive. Consider replacing laminate countertops with granite and replacing a sink and faucet, for example. Leave cabinet boxes in place but replace out-of-date doors and hardware ‒ or hire a professional to give doors and drawers a fresh coat of paint. Finally, you can replace older appliances with slide-in, energy-efficient, stainless steel models. It’s your call as to whether spending money on these kitchen redo’s is feasible; think about your individual circumstances and what your goal is for selling your home. It also may be helpful to contact your homeowners insurance representative, to make sure that any renovations you’re considering will be covered. A savvy refresh doesn’t have to include all kitchen elements. Instead, to help save on cost, pick and choose the features that can make the greatest impression within your space. 6. Deep clean and declutter. When it comes to selling a home, you want to make a great first impression. Messy playrooms, cat or dog odors (even if Fido isn’t home), or an unmade bed can all be a turnoff to potential homebuyers. That may be why many real estate agents suggest their clients declutter and deep clean before listing their house for sale. While the main living spaces should take center stage, potential homebuyers may open your cabinets, drawers and refrigerator, so be sure to give them a good once-over, too. 7. Hire a professional home stager. When it comes down to it, the buyers who can envision themselves living in your home are the ones most likely to buy. That’s why staging your home to sell is such a popular tactic. A professional home stager will suggest removing personal items like photographs and excess furniture. Many professionals suggest storing or removing a quarter to half of your possessions, including sofas, bookcases, knickknacks, books and even clothes in your closet. Still, removing excess stuff is just the start. Stagers may rearrange furniture to highlight features like the fireplace, a view or unique architectural details. They may even suggest that you use a rental service to bring in items to dress up your home and will arrange for that service if you decide to take that advice. A professional home stager will often cost several hundred dollars, but the investment can help a home sell faster ‒ and often at a higher price than similar homes. To get the biggest bang for your staging buck, stagers recommend focusing on the living room, master bedroom and kitchen, in that order. 8. A fresh coat of interior paint. Paint has the power to entirely transform a home, particularly if it’s been a while since you upgraded your color scheme or if you happen to love eclectic colors. Neutrals are typically a safe bet ‒ they can create that clean slate feel that give home shoppers a greater ability to see their own belongings in your space. 9. Optimize lighting. High-quality lighting can help make a room feel larger, more modern and more inviting to potential homebuyers. For daytime showings, open curtains and blinds to bring in as much natural light as you can. Take advantage of accent lighting throughout the day and evening to emphasize art, a reading nook or any other interesting features in your home. If your home still feels dark, try strategically placing a mirror to reflect light and help make a room appear brighter. Alternatively, you can help brighten your space by bringing in a stylish floor or table lamp. If your fixtures are dated, new dining room and foyer chandeliers can bring a more modern vibe to your space. 10. Make small repairs. You may be accustomed to the inconvenience of that torn window screen or leaky showerhead but, to a new potential homebuyer, they may be red flags, prompting them to stay alert for any other necessary but unmade home repairs they’ll have to consider when it comes time to make an offer. Help get ahead of potential problems by doing a walkthrough, looking for any damage or necessary repairs. Then, consider hiring a handyman for the day. To really head off problems, consider hiring your own home inspector to help alert you to unexpected issues you can repair before homebuyers start walking through your home. Before You Move, Review Your Homeowner’s Insurance Coverage Selling your home is a good time to review your homeowners coverage. Learn more with us at: 508-540-2601  Maybe you’ve heard that people who drive red cars get pulled over more, so insurers charge them higher rates. Or that if you let someone else drive your car, their policy will cover an accident.

Well, when it comes to auto insurance, you shouldn’t always believe what you hear. Get the facts about common car insurance myths, and reach out to make sure you have the coverage you need. Myth #1: A ticket automatically increases your rate. A moving violation doesn't have to increase your insurance rate unless it's a frequent occurrence. You may be able to take a driving course to maintain your rate and even pay less for your ticket. Myth #2: Car color affects your insurance rate. The truth is that the color of your vehicle most likely doesn’t affect your premiums. However, there are special cases where color can raise the value of your car — like a custom paint job — which could potentially increase your rates. Myth #3: Older cars need less coverage. If you don't have a loan on your car, you may not have to carry comprehensive and collision coverage, only the liability coverage required by the state. But you may not want to drop or lower your optional coverage if your car still has significant value, as it would be pricey to repair or replace. Myth #4: Someone borrowing your vehicle is covered by their own insurance. Laws vary by state, but usually the insurance covers the vehicle. Before you drive someone else's car, verify that it's insured. Don't assume that your own policy will cover an accident. Myth #5: You only need the auto liability insurance that's required by law. It's smart to buy more than the minimum, because personal liability for an at-fault auto accident can be expensive. Adding a personal umbrella policy for additional coverage can be a wise decision, especially when you have assets to protect. Get in touch today with any questions you have about your policy.  Even a perfectly planned budget can be thrown off track by a surprise expense. That's why you've carefully set aside savings in your emergency fund.

But what kind of situation can warrant dipping into that fund? Since you've dedicated that money to emergencies, you owe it to yourself to make sure you spend it wisely. From unexpected car repairs to home maintenance, here's when you should use your savings. Job Loss If you unexpectedly lose your job, you still need to pay the bills. Your emergency fund provides you a cushion to keep up with your expenses as you decide what's next for your career. Car Issues What happens if your car breaks down? First, you'll need to pay your car insurance deductible and figure out any additional expenses related to repairs and a rental. Then, your savings can keep you on the road while your vehicle is in the shop. Home Damage Storm or flooding destruction to your home may require repairs as soon as possible. Your emergency fund is there to cover your home insurance deductible and any additional expenses related to the damage. Where Not to Spend Your Emergency Fund Remember: Not every unexpected expense counts as an emergency. For example, if you have the opportunity to go on an exciting trip or decide you want to upgrade your phone to a new model, it probably doesn't make sense to pay for those purchases from your emergency fund. In addition to your savings, you have insurance to help protect your belongings and your financial security. Get in touch to talk about your car and home coverage. Together, we can discuss your benefits and any potential updates.  How clean is your car? If you don’t wash it regularly, you could end up with costly maintenance and safety issues.

You might occasionally run your vehicle through a car wash. But there are benefits to doing the job yourself — including preserving the paint and being able to get into every nook and cranny. Ready to get started? Follow these five tips to wash your car thoroughly and correctly.

|

better Insurance

|

RSS Feed

RSS Feed

Arthur D. Calfee Insurance Agency, Inc. is a friendly local insurance agency proudly offering Massachusetts, Cape Cod and the Islands. A-Excellent AM Best rating, A+ Excellent by the BBB

Using innovative thinking, cutting-edge tools and expert resources at national and local levels, we deliver the best possible outcome on every policy we manage. Need Home Insurance? Easy, Fast, & Secure Home Insurance. Get Free Quotes 100% Online Now! Available 24/7. Affordable Rates. Cover Your Biggest Investments. Get a homeowners insurance quote, find coverage options. We'll help you understand and customize the right home insurance coverage for you.

Home is where your heart is—along with a healthy chunk of your net worth. Get started today with a free homeowner's quote.

Compare home insurance quotes today and save on protection for your biggest investment. Build a Custom Policy & Make the Switch! Our local underwriting professionals focus exclusively on finding the best home insurance, homeowner's insurance, hazard insurance, investment property insurance, flood insurance, flood zone information, vacation home insurance, second home insurance, auto insurance, collector car insurance, business insurance, general liability insurance, property insurance, professional liability insurance, contractor's liability insurance, worker's comp insurance, key man insurance, whole life insurance, term life insurance, group or personal disability, & long-term care insurance policies to patrons in the following Cape Cod, Massachusetts towns, communities and villages: Barnstable, Bourne, Pocasset, Brewster, Buzzards Bay, Centerville, Chatham, Cotuit, Craigville, Dennis, East Dennis, Eastham, Falmouth, East Falmouth, Hatchville, West Falmouth, North Falmouth, Woods Hole, Harwich, Hyannis, Hyannisport, Martha's Vineyard, Nantucket, Marstons Mills, Mashpee, Orleans, Osterville, Provincetown, Sandwich, Sagamore, Sagamore Beach, Truro, Wellfleet, Yarmouth, and Yarmouthport. Real-Time Pricing. Insurance coverage: Wind Damage, Fire Loss, Water Damage. Protect your home and belongings. Low Rates For Your Best Options to Save Money On Great Coverage! Get a quote today. Home insurance helps protect your house and your family.

Using innovative thinking, cutting-edge tools and expert resources at national and local levels, we deliver the best possible outcome on every policy we manage. Need Home Insurance? Easy, Fast, & Secure Home Insurance. Get Free Quotes 100% Online Now! Available 24/7. Affordable Rates. Cover Your Biggest Investments. Get a homeowners insurance quote, find coverage options. We'll help you understand and customize the right home insurance coverage for you.

Home is where your heart is—along with a healthy chunk of your net worth. Get started today with a free homeowner's quote.

Compare home insurance quotes today and save on protection for your biggest investment. Build a Custom Policy & Make the Switch! Our local underwriting professionals focus exclusively on finding the best home insurance, homeowner's insurance, hazard insurance, investment property insurance, flood insurance, flood zone information, vacation home insurance, second home insurance, auto insurance, collector car insurance, business insurance, general liability insurance, property insurance, professional liability insurance, contractor's liability insurance, worker's comp insurance, key man insurance, whole life insurance, term life insurance, group or personal disability, & long-term care insurance policies to patrons in the following Cape Cod, Massachusetts towns, communities and villages: Barnstable, Bourne, Pocasset, Brewster, Buzzards Bay, Centerville, Chatham, Cotuit, Craigville, Dennis, East Dennis, Eastham, Falmouth, East Falmouth, Hatchville, West Falmouth, North Falmouth, Woods Hole, Harwich, Hyannis, Hyannisport, Martha's Vineyard, Nantucket, Marstons Mills, Mashpee, Orleans, Osterville, Provincetown, Sandwich, Sagamore, Sagamore Beach, Truro, Wellfleet, Yarmouth, and Yarmouthport. Real-Time Pricing. Insurance coverage: Wind Damage, Fire Loss, Water Damage. Protect your home and belongings. Low Rates For Your Best Options to Save Money On Great Coverage! Get a quote today. Home insurance helps protect your house and your family.

Testimonials & Endorsements for the Best Insurance Agent on Cape Cod, MA

PHONE: (800) 479-2601 CUSTOMER SUPPORT & SERVICE

Please note: The above is meant as general information to help you understand the different aspects of insurance. This information is not an insurance policy, does not refer to any specific insurance policy, and does not modify any provisions, limitations, or exclusions expressly stated in any insurance policy. Descriptions of all coverages and other features on this page are necessarily brief; in order to fully understand the coverages and other features of a specific insurance policy, we encourage you to read the applicable policy and/or speak to an insurance representative. Coverages and other features vary between insurers, vary by state, and are not available in all states. Whether an accident or other loss is covered is subject to the terms and conditions of the actual insurance policy or policies involved in the claim. References to average or typical premiums, amounts of losses, deductibles, costs of coverages/repair, etc., are illustrative and may not apply to your situation. We are not responsible for the content of any third-party sites linked from this page.

© 2024 Copyright, Arthur D. Calfee Insurance Agency, Inc.

Calfee Cares.® Privacy Policy

Calfee Cares.® Privacy Policy