When it comes to home repairs and renovations, it can be difficult to know what you can accomplish on your own — and which projects are best handled by a trained professional.

Costs, safety, time and the finished product are all things you should plan around. Consider the pros and cons of doing it yourself versus hiring a professional for a project. You may be able to do smaller things on your own, but some jobs are better left to an expert. What’s the time commitment? Thanks to online tutorials, you have access to near-infinite home repair knowledge. But how much time do you actually have to put that information into action? Before starting a DIY project, make sure you can complete the work within your target timeframe. For example, if you need to get a nursery ready before a new baby is born, can you expect to meet that deadline? Are you okay with spending so much of your spare time on it? How much will you save? Since you’re not paying someone else for their labor, you should be able to save a ton of money on your home project, right? The answer isn’t always that simple. For example, do you already have the tools and materials you need? You can always get a few quotes to compare the expense of hiring a professional. And keep in mind that you may have to hire a pro if there are issues, meaning extra spending on top of the money you’ve already invested into it. Is safety an issue? A good rule of thumb is that any project requiring a permit might be too big or too risky to DIY. This includes electricity, plumbing, digging and structural changes. It’s not worth the chance that a mistake could hurt you or make your home unsafe. Can you accept “good enough” instead of perfect? Let’s face it: Sometimes a finished DIY project doesn’t look as good as if a contractor did it. If you want a renovation to come out perfectly (or if you want to sell your home quickly), consider hiring a professional. Have questions about your home insurance and how your coverage can be affected by renovations? Reach out for assistance.

0 Comments

Are you missing out on savings? If you have insurance policies with more than one company, the answer is most likely yes.

The commercials are true: Bundling insurance policies is often cheaper and more convenient when done with a single insurer. But why? While bundling may not be right for everyone, here is the how – and the why – on insurance bundling. Then you can make your own decision. What does it mean to bundle my home and auto insurance? Bundling your home (or renter’s) and auto insurance means getting both policies from the same insurer. You can ask for a quote to see your potential savings before you make a switch. 1. Save money when you bundle policies. You probably have to have home and auto insurance anyway, so you want to get the best possible deal on your coverage. You may be eligible for a multipolicy discount when you get more than one insurance policy from the same company. This is in addition to any other discounts you receive, such as for a good driving record. 2. Simplify payments and organization. Bundling your insurance coverage can help you simplify with one monthly payment instead of several. It’s also easier to keep up with your policies when you can view all your insurance documents in one place. Check your coverage, ask a question, and file a claim — all from the same online portal or mobile app. If your insurance needs to change in the future, you just have one phone call to make. 3. Increase your convenience as a customer. If you file claims often, it's better to have a company that knows and values you as a customer. And even if you don’t file many claims, holding multiple policies with a single insurer gives more business to a company that has given you superior customer service in the past. If you have any questions, reach out for help.  Do you have uninvited guests in your home? Depending on where you live, pests could be a year-round or seasonal issue, but they are never welcome. Nothing shatters your sense of peace and comfort in your home like discovering mice, termites, ants or other pests looking for food and shelter.

Luckily, there are tried-and-true methods for dealing with bugs and rodents in both the short and long terms. Keep reading to discover the best pest control solutions for your home. Short-Term Pest Control Solutions Once you’ve spotted signs of an infestation in your home, here’s what you can do to control the problem immediately:

Once you get things under control for now, you’ll want to address the root cause to keep pests away for the long run.

While no one enjoys dealing with pest issues, regular maintenance and prevention can help keep your home a haven — but only for you and your human guests. Have questions about homeownership or insurance? Reach out so we can discuss your coverage.  We know that many of our customers are continuing to do their part to help stop the spread of COVID-19 by staying at home. Even as more states begin to relax their shelter-in-place orders, many people continue to drive fewer miles, resulting in a decrease in auto claims. With that in mind, we are extending our Stay-at-Home Auto Premium Credit Program, which will automatically give our Travelers Insurance customers a 15% credit on their June auto premiums. Customers will receive the automatic credit either on future bills or via their last payment method. Answers to questions that you may have about this program can be found here. The extension of our Stay-at-Home Auto Program is another example of our efforts to provide relief during this challenging time. For our Travelers Insurance customers, other initiatives include suspending cancellation and nonrenewal of coverage due to nonpayment through June 15 – there will be no interest, late fees or penalties charged during this time. We have pledged $5 million to COVID-19 relief efforts to assist families and communities across North America, the United Kingdom and the Republic of Ireland.   Auto & Home Bundle Quote 508-540-2601Get a quote online and work with an insurance agent to find the right Home Insurance coverage for your property and unique needs. Cover Your Biggest Investments. Get a homeowners insurance quote, find coverage options. We'll help you understand and customize the right home insurance coverage for you.      We recommend coverage amounts for your personal situation and break down everything we offer with clear-cut explanations so you know exactly what you’re getting. When purchasing property, doing your due diligence is more than a turn of phrase. The period when a house is under contract is an essential part of the homebuying process and requires careful attention to detail. By answering some simple questions about your home, we’ll get you the protection that you deserve, all through our secure network. We recommend coverage amounts for your personal situation and break down everything we offer with clear-cut explanations so you know exactly what you’re getting. The Basics The due diligence process is the buyer's opportunity to review all facets of a potential home sale. From home inspection findings to homeowner insurance costs, it's when you'll take the time to understand exactly what you're potentially buying. Here are a few due diligence do's and don'ts to consider: Do find out how long it lasts. Two weeks is fairly standard for the average due diligence process. However, shorter periods may be negotiated to gain a competitive edge in a seller's market. Don't make assumptions about when it begins. In some cases, due diligence is conducted before a property goes under contract. In others, it begins after the contract is signed. Do consult an insurance agent. Floodplain and fire-prone areas may require additional coverage. Make sure you know the estimated costs and what a new homeowners insurance policy will cover. Don't skim the home inspection. Make sure you're familiar with every line of the report. You may want to get quotes from contractors or negotiate repair costs into your offer. Do your research. Review neighborhood characteristics and check the area's crime rates. Look at zoning laws to ensure they align with your long-term goals. Don't forget to review the HOA. If you're joining a homeowners association, it's not enough to simply read your HOA documents. Make sure the community is in good physical condition and the association is financially sound. Being thorough in the due diligence phase will help you uncover potential issues and make the right choices for you and your family.

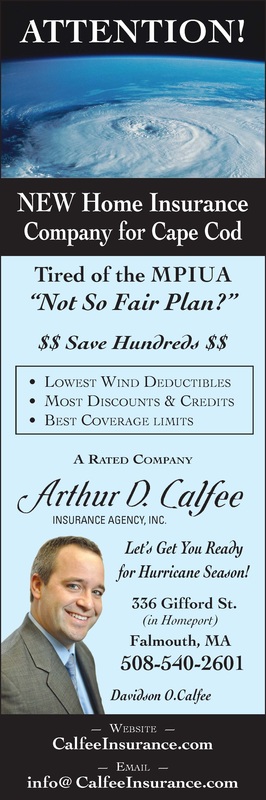

This just in... there is a new Home Insurance Program available to Massachusetts residents that was just approved by the Massachusetts Commissioner of Insurance. This is an A Rated Company by AM Best and specializing in Home Insurance near the ocean. They have chosen the Arthur D. Calfee Insurance Agency, with their corporate office located in Falmouth, on Cape Cod, in Massachusetts, to be their Home Insurance Representative Agent. Find out if you qualify for this new Home Insurance Program by calling 508-444-0509 or get a Quick Online Home Insurance Quote at www.CalfeeInsurance.com Actual cash value or replacement cost?

When it comes to insuring your most valuable possessions, you have important choices to make. In the event of a loss involving your home or car, do you know how you'd like to be reimbursed? Does your current policy reflect these preferences? Carefully evaluate these two types of coverage to ensure you're well-informed. Actual Cash Value If you elect for an actual cash value insurance policy, you'll likely be compensated for the fair market value of the item at the time it was lost or damaged. Pro: These policies often have less expensive monthly premiums, so you could insure expensive items for less. Con: The payout is not based on what you paid for the item. This means you could be out the difference if something has depreciated in value since you purchased it. For example, if you had a wreck and wanted to replace the car you bought five years ago, you'll probably be accepting payment for what a vehicle of that make and model would fetch now, minus your deductible and wear and tear. Replacement Cost Many agents recommend replacement cost insurance, especially for homeowners. This sets you up to be reimbursed for the full amount it would take to rebuild your home and replace everything in it. Pro: You can replace older items for what they would cost to purchase new. Con: This option tends to be more expensive. Also, you must replace all items claimed to recoup the payout and you can't use the money for other things. Keep in mind that multiple factorscome into play when determining how an insurance claim will be paid out, but by learning about your options you can set yourself up for success. Please reach out with any questions you have.  Universal Insurance Holdings, Inc. ("UIH" or the "Company") was organized as Universal Heights, Inc. in 1990. The Company changed its name to Universal Insurance Holdings, Inc. on January 12, 2001. In April 1997, the Company organized a subsidiary, Universal Property & Casualty Insurance Company ("UPCIC"), as part of its strategy to take advantage of growth opportunities in the Florida homeowners’ insurance marketplace. UPCIC was formed to participate in the transfer of homeowners' insurance policies from the Florida Residential Property and Casualty Joint Underwriting Association ("JUA"). The Company has since evolved into a vertically integrated insurance holding company, which through its various subsidiaries, covers substantially all aspects of insurance underwriting, distribution, claims processing and exposure management. Universal Insurance Holdings, Inc. (UIH), with its wholly-owned subsidiaries, is a vertically integrated insurance holding company performing all aspects of insurance underwriting, distribution and claims. Universal Property & Casualty Insurance Company (UPCIC), a wholly owned subsidiary of the Company, is one of the three leading writers of homeowners insurance in Florida and is now fully licensed and has commenced its operations in Alabama, Delaware, Florida, Georgia, Hawaii, Indiana, Maryland, Massachusetts, Michigan, Minnesota, North Carolina, Pennsylvania, and South Carolina. American Platinum Property and Casualty Insurance Company (APPCIC), also a wholly owned subsidiary, currently writes homeowners multi-peril insurance on Florida homes valued in excess of $1 million, which are limits and coverages currently not targeted through its affiliate UPCIC. UIH’s insurance company subsidiaries have established strong relationships with a network of over 8,000 independent agents by emphasizing personal interaction, offering superior services and maintaining an exclusive focus on homeowners insurance. The Company’s insurance company underwriters work closely with independent agents to market and underwrite business. With competitively priced products, convenient installment billing plans and proactive claims management, both UPCIC and APPCIC provide their customers with superior service. At December 31, 2015, UIH's insurance company subsidiaries serviced approximately 624 thousand homeowners and dwelling fire insurance policies. Management Structure Sean P. Downes Chairman and Chief Executive OfficerSean P. Downes has been Chairman of the Board of Directors and Chief Executive Officer of the Company since 2013 and a director of the Company since 2005. Mr. Downes also served as President of the Company from 2013 until March 2016. Prior to serving in these roles, he served as Senior Vice President and Chief Operating Officer of the Company since 2005 and Chief Operating Officer and a director of UPCIC, a wholly-owned subsidiary of the Company, since 2003. Mr. Downes was Chief Operating Officer of Universal Adjusting Corporation from 1999 to 2003. During that time, Mr. Downes created the Company's claims operation. Before joining the Company in 1999, Mr. Downes was Vice President of Downes and Associates, a multi-line insurance claims adjustment corporation. Jon W. Springer President and Chief Risk OfficerJon W. Springer has been President and Chief Risk Officer of the Company since March 2016 and a director of the Company since 2013. Mr. Springer has held several senior leadership positions with increasing responsibility at the Company, and has been instrumental in the development of the Company’s reinsurance programs and operations. Prior to assuming the positions of President and Chief Risk Officer, Mr. Springer served as Executive Vice President and Chief Operating Officer of the Company since 2013. Previously, Mr. Springer was Executive Vice President of Blue Atlantic Reinsurance Corporation, a wholly-owned subsidiary of the Company, from 2008 to 2013, and Executive Vice President of Universal Risk Advisors, Inc., a wholly-owned subsidiary of the Company, from 2006 to 2008. Before joining Universal Risk Advisors, Inc., Mr. Springer was an Executive Vice President of Willis Re, Inc. and was responsible for managing property and casualty operations in its Minneapolis office. Stephen J. Donaghy Chief Operating OfficerStephen J. Donaghy has been Chief Operating Officer of the Company since March 2016. Mr. Donaghy has held key senior leadership roles in the areas of operations, marketing, sales and corporate strategy throughout his career. Prior to assuming the position of Chief Operating Officer, Mr. Donaghy served as the Company’s Chief Marketing Officer, a position he held starting in January 2015. Mr. Donaghy previously served as the Company’s Chief Administrative Officer from 2013 to June 2015, Chief Information Officer from 2009 to 2013 and Executive Vice President from 2006 to 2009. Before joining the Company, Mr. Donaghy held various executive positions at JM Family Enterprises, a top 100 Forbes private company in the United States; including Vice President of Strategic Initiatives, Vice President of Sales and Marketing and Senior Information Officer. Frank Wilcox Chief Financial Officer and Principal Accounting OfficerFrank C. Wilcox became Chief Financial Officer and Principal Accounting Officer of the Company and its wholly-owned insurance subsidiaries in 2013. Prior to this role, he served as the Company's Vice President - Finance since 2011. Before joining the Company, Mr. Wilcox was Director, Consolidation and SEC Reporting at Burger King Corporation from 2006 to 2011. From 2000 to 2006, he served as Senior Vice President, Controller at BankUnited. Earlier in his career he served in various capacities within the financial services industry, which included a role as an auditor at a large public accounting firm. Mr. Wilcox has been licensed as a certified public accountant in New York since 1996. Kimberly D. Cooper Chief Information OfficerKimberly D. Cooper became the Chief Administrative Officer of the Company in June 2015 and the Chief Information Officer of the Company in February 2015. Prior to assuming these roles, Ms. Cooper spent eight years in the Company’s IT department, serving as both IT Manager and then IT Audit Director. She managed new application deployment and performed ongoing security and risk awareness training to improve operational efficiencies and ensure ongoing compliance with regulatory requirements. Before joining the Company, Ms. Cooper supervised audit and assurance engagements for Fortune 500 clients in the financial services industry, both domestically and internationally, as part of the systems and process assurance practice at PricewaterhouseCoopers (PwC). She has been licensed as a Certified Information Security Auditor (CISA) and Certified in Risk and Information Security Controls (CRISC) since December of 2007. Ms. Cooper holds a Bachelor of Science degree from University of California, Berkeley. |

Real EstateStay up to date on Cape Cod Real Estate! Land for Sale, Water Front Properties & more!

Register now for free email updates of new listings matching your home search.

Auto Insurance

Homeowners Insurance Condo Insurance Renters Insurance Rental Home Insurance Rental Condo Insurance Landlord Insurance Motorcycle Insurance Personal Umbrella Policy Earthquake Insurance Flood Insurance Off Road Vehicles Motor Home Insurance Mobile Home Insurance Travel Trailer Insurance Recreational Vehicles Boat & Yacht Insurance Jet Ski Insurance Personal Watercraft Snowmobile Insurance

Archives

September 2023

Categories

All

Arthur D. Calfee Insurance Agency, Inc. is proudly serving primary home, vacation home, auto, collector car, business, general liability, property, professional liability, contractor's liability, worker's comp, key man, whole life, term life, group or personal disability, & long-term care insurance policies to patrons in the following Cape Cod, Massachusetts towns, communities and villages: Barnstable, Bourne, Brewster, Buzzards Bay, Centerville, Chatham, Cotuit, Craigville, Dennis, Eastham, Falmouth, Hatchville, Harwich, Hyannis, Hyannisport, Marstons Mills, Mashpee, Orleans, Osterville, Provincetown, Sandwich, Truro, Wellfleet, Woods Hole, Yarmouth, and Yarmouthport.

Cape Cod Home Insurance for Coastal Properties

*Lowest Wind Deductibles

*Most Discounts & Credits

*Best Coverage Limits

|

RSS Feed

RSS Feed

Arthur D. Calfee Insurance Agency, Inc. is a friendly local insurance agency proudly offering Massachusetts, Cape Cod and the Islands. A-Excellent AM Best rating, A+ Excellent by the BBB

Using innovative thinking, cutting-edge tools and expert resources at national and local levels, we deliver the best possible outcome on every policy we manage. Need Home Insurance? Easy, Fast, & Secure Home Insurance. Get Free Quotes 100% Online Now! Available 24/7. Affordable Rates. Cover Your Biggest Investments. Get a homeowners insurance quote, find coverage options. We'll help you understand and customize the right home insurance coverage for you.

Home is where your heart is—along with a healthy chunk of your net worth. Get started today with a free homeowner's quote.

Compare home insurance quotes today and save on protection for your biggest investment. Build a Custom Policy & Make the Switch! Our local underwriting professionals focus exclusively on finding the best home insurance, homeowner's insurance, hazard insurance, investment property insurance, flood insurance, flood zone information, vacation home insurance, second home insurance, auto insurance, collector car insurance, business insurance, general liability insurance, property insurance, professional liability insurance, contractor's liability insurance, worker's comp insurance, key man insurance, whole life insurance, term life insurance, group or personal disability, & long-term care insurance policies to patrons in the following Cape Cod, Massachusetts towns, communities and villages: Barnstable, Bourne, Pocasset, Brewster, Buzzards Bay, Centerville, Chatham, Cotuit, Craigville, Dennis, East Dennis, Eastham, Falmouth, East Falmouth, Hatchville, West Falmouth, North Falmouth, Woods Hole, Harwich, Hyannis, Hyannisport, Martha's Vineyard, Nantucket, Marstons Mills, Mashpee, Orleans, Osterville, Provincetown, Sandwich, Sagamore, Sagamore Beach, Truro, Wellfleet, Yarmouth, and Yarmouthport. Real-Time Pricing. Insurance coverage: Wind Damage, Fire Loss, Water Damage. Protect your home and belongings. Low Rates For Your Best Options to Save Money On Great Coverage! Get a quote today. Home insurance helps protect your house and your family.

Using innovative thinking, cutting-edge tools and expert resources at national and local levels, we deliver the best possible outcome on every policy we manage. Need Home Insurance? Easy, Fast, & Secure Home Insurance. Get Free Quotes 100% Online Now! Available 24/7. Affordable Rates. Cover Your Biggest Investments. Get a homeowners insurance quote, find coverage options. We'll help you understand and customize the right home insurance coverage for you.

Home is where your heart is—along with a healthy chunk of your net worth. Get started today with a free homeowner's quote.

Compare home insurance quotes today and save on protection for your biggest investment. Build a Custom Policy & Make the Switch! Our local underwriting professionals focus exclusively on finding the best home insurance, homeowner's insurance, hazard insurance, investment property insurance, flood insurance, flood zone information, vacation home insurance, second home insurance, auto insurance, collector car insurance, business insurance, general liability insurance, property insurance, professional liability insurance, contractor's liability insurance, worker's comp insurance, key man insurance, whole life insurance, term life insurance, group or personal disability, & long-term care insurance policies to patrons in the following Cape Cod, Massachusetts towns, communities and villages: Barnstable, Bourne, Pocasset, Brewster, Buzzards Bay, Centerville, Chatham, Cotuit, Craigville, Dennis, East Dennis, Eastham, Falmouth, East Falmouth, Hatchville, West Falmouth, North Falmouth, Woods Hole, Harwich, Hyannis, Hyannisport, Martha's Vineyard, Nantucket, Marstons Mills, Mashpee, Orleans, Osterville, Provincetown, Sandwich, Sagamore, Sagamore Beach, Truro, Wellfleet, Yarmouth, and Yarmouthport. Real-Time Pricing. Insurance coverage: Wind Damage, Fire Loss, Water Damage. Protect your home and belongings. Low Rates For Your Best Options to Save Money On Great Coverage! Get a quote today. Home insurance helps protect your house and your family.

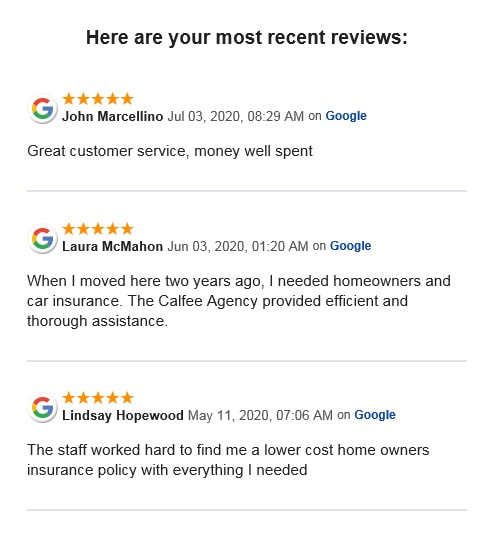

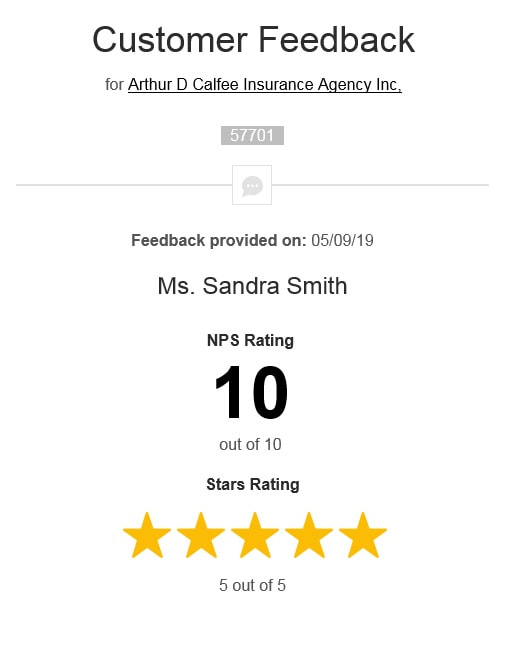

Testimonials & Endorsements for the Best Insurance Agent on Cape Cod, MA

PHONE: (800) 479-2601 CUSTOMER SUPPORT & SERVICE

Please note: The above is meant as general information to help you understand the different aspects of insurance. This information is not an insurance policy, does not refer to any specific insurance policy, and does not modify any provisions, limitations, or exclusions expressly stated in any insurance policy. Descriptions of all coverages and other features on this page are necessarily brief; in order to fully understand the coverages and other features of a specific insurance policy, we encourage you to read the applicable policy and/or speak to an insurance representative. Coverages and other features vary between insurers, vary by state, and are not available in all states. Whether an accident or other loss is covered is subject to the terms and conditions of the actual insurance policy or policies involved in the claim. References to average or typical premiums, amounts of losses, deductibles, costs of coverages/repair, etc., are illustrative and may not apply to your situation. We are not responsible for the content of any third-party sites linked from this page.

© 2023 Copyright, Arthur D. Calfee Insurance Agency, Inc.

Calfee Cares.® Privacy Policy

Calfee Cares.® Privacy Policy